Rotation Absorbs the Fed, Not the Headlines

Gold and Silver fell off a cliff - and the SPX shrugged

Beyond the Noise

Rotation Absorbs the Fed, Not the Headlines

February 1, 2026

Market Recap — The Fed Didn’t Break the Range

U.S. equities finished the week little changed at the index level, but once again, the surface-level calm masked meaningful cross-currents underneath.

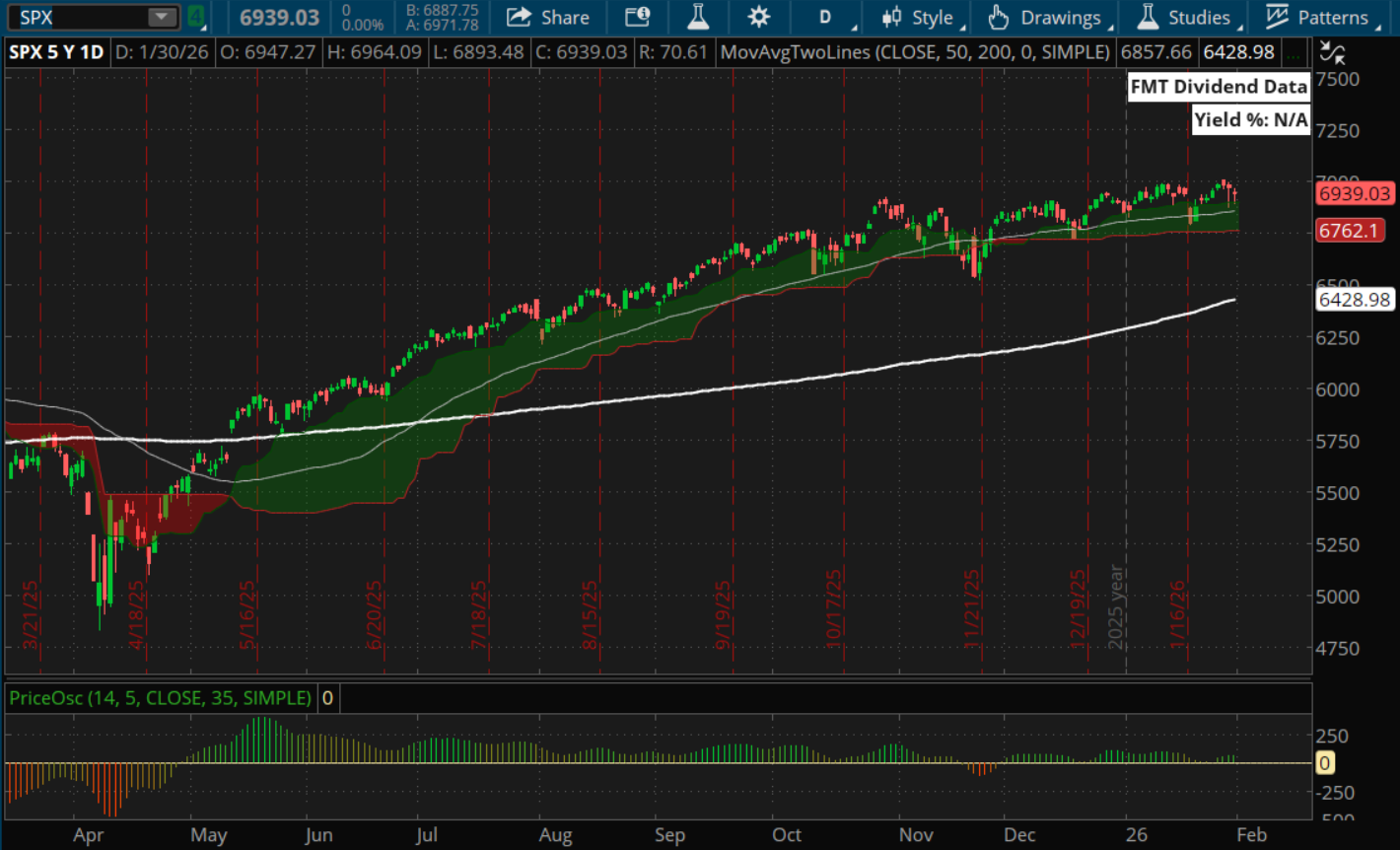

The S&P 500 continued to churn in a tight range near highs, digesting gains rather than extending them. That consolidation survived a full slate of potential catalysts — the FOMC decision, major earnings, political headlines, and a sharp move in commodities — without breaking trend.

That’s not accidental. It’s a market still reallocating, not unraveling.

Rotation remains the dominant force.

Fed Decision — Hold Was Expected, Tone Was the Story

The Fed delivered exactly what markets expected: no rate change. The reaction, however, was shaped by nuance rather than the decision itself.

Key takeaways from the meeting and press conference:

• The Committee reinforced a data-dependent posture, avoiding any firm commitment on timing

• Inflation progress was acknowledged, but not declared “complete”

• Labor market resilience remains central to the Fed’s confidence

• The tone leaned patient, not urgent

In short: no pivot, no panic, no surprise.

That matters. A Fed that is comfortable waiting — rather than rushing to cut — keeps financial conditions tight enough to restrain speculation but loose enough to support selective risk-taking.

The market heard that message and largely shrugged.

Political Noise — Trump’s Fed Nomination Headlines

Midweek, markets also digested news around former President Trump’s announced nomination preference for a future Federal Reserve role.

The immediate takeaway wasn’t policy — it was uncertainty. Markets generally dislike guessing games around central bank independence, but in this case, price action suggested restraint rather than alarm.

Equities barely flinched. Rates held their range.

This reinforces an important theme: political headlines matter less when monetary policy is already constrained by data and inflation math. Until the outlook materially changes, the market appears unwilling to overreact.

Commodities — Gold and Silver Lose Their Bid

One of the more notable moves last week came outside equities.

Gold and silver both sold off meaningfully as:

• Real yields firmed modestly

• The Fed avoided signaling imminent cuts

• Risk assets remained supported

This wasn’t a collapse — but it was a reminder that precious metals need either accelerating inflation fears or aggressive easing expectations to sustain upside.

In a “patient Fed, resilient economy” environment, those tailwinds weaken.

Earnings Recap — Confirmation, Not Acceleration

Earnings continued to reinforce the broader rotation narrative.

What stood out wasn’t disaster — it was dispersion:

• Mega-cap growth names largely met expectations but struggled to expand multiples

• Industrials and cyclicals delivered solid results, with mixed guidance

• Margin commentary mattered more than revenue beats

The market rewarded companies with visible cash flow durability and punished crowded trades with little room for error.

Again: not risk-off — selective.

Looking Ahead — Shutdown Noise, Data Reality

Federal Shutdown

Washington headlines will likely focus on the looming federal shutdown early this week. At the moment, markets are treating this as short-lived political theater, not a systemic risk.

Unless it drags on materially longer than expected, history suggests market impact should remain limited.

Notable Earnings This Week — Guidance Over Headlines

Earnings season continues to do more confirming than catalyzing, but this week’s lineup still matters for rotation and leadership signals.

🗓 Earnings to Watch

Monday

Palantir (PLTR) – sentiment read on AI-adjacent government and enterprise spending

McDonald’s (MCD) – global consumer demand and pricing power

Tuesday

Alphabet (GOOGL) – digital advertising trends and AI monetization

Uber (UBER) – consumer mobility and discretionary spending

Ford (F) – pricing discipline and EV margin commentary

Wednesday

Amazon (AMZN) – consumer demand, cloud growth, and cost control

Qualcomm (QCOM) – handset demand and semiconductor cycle positioning

Thursday

Disney (DIS) – streaming profitability and media stabilization

PepsiCo (PEP) – defensive consumer spending and margin resilience

Friday

Exxon Mobil (XOM) / Chevron (CVX) – energy cash flow discipline and capital return

🧠 What the Market Will Listen For

This week is less about beats and misses and more about forward visibility:

Do mega-cap tech names reaccelerate — or simply hold ground?

Do consumer-facing companies confirm resilience without margin erosion?

Do energy and industrials reinforce cash-flow durability over growth narratives?

Strong results may be rewarded selectively, but crowded positioning means execution matters more than optimism.

In this environment, earnings that reduce uncertainty tend to matter more than earnings that merely beat estimates.

If you want, I can also:

Economic Calendar — Quiet, But Not Irrelevant

This week’s calendar includes:

• ISM Manufacturing & Services

• JOLTS

• ADP Employment

• Friday’s jobs report

None of these are likely to change Fed policy on their own — but together they shape the patience narrative. Strong data keeps cuts delayed. Weak data pulls expectations forward.

Markets will trade the direction, not the print.

Technical Context — Still a Range, Still Constructive

Technically, nothing changed.

The S&P 500 remains:

• Above its rising 50-day

• Locked in a consolidation range

• Supported on dips, capped on strength

That’s the textbook definition of digestion.

Until the 50-day breaks decisively, the primary trend remains intact — but sideways.

🎯 Trader’s Playbook

• Expect continued index chop

• Don’t overreact to headlines

• Respect rotation and dispersion

• Favor stock-specific catalysts

• Avoid chasing crowded trades

• Let price — not prediction — lead

This remains a market where patience is rewarded and urgency is punished.

Sideways indexes frustrate traders who need action — but they quietly favor those willing to wait for asymmetric opportunities to develop beneath the noise.

Spot on framing with the "patience rewarded, urgency punished" angle. I'm seeing that playbook everywere lately, where the index flatness hides a ton of action underneath. Your observation about gold/silver losing the bid while equities barely blinked is really telling. When safe havens selloff but risk assets hold steady, it suggests people are rotating into what's working not fleeing to safety. Watched similar patterns in 2017 before the breakout.