No Deal? No Problem — For Now

Headlines Create Worry. Price Creates Wealth.

Beyond the Noise

June 1, 2026

No Deal? No Problem — For Now

The market spent another week doing something that continues to frustrate both bears and skeptics:

Ignoring reasons to go down.

Iran negotiations remain unresolved.

Geopolitical headlines continue to shift almost daily.

Economic growth remains mixed.

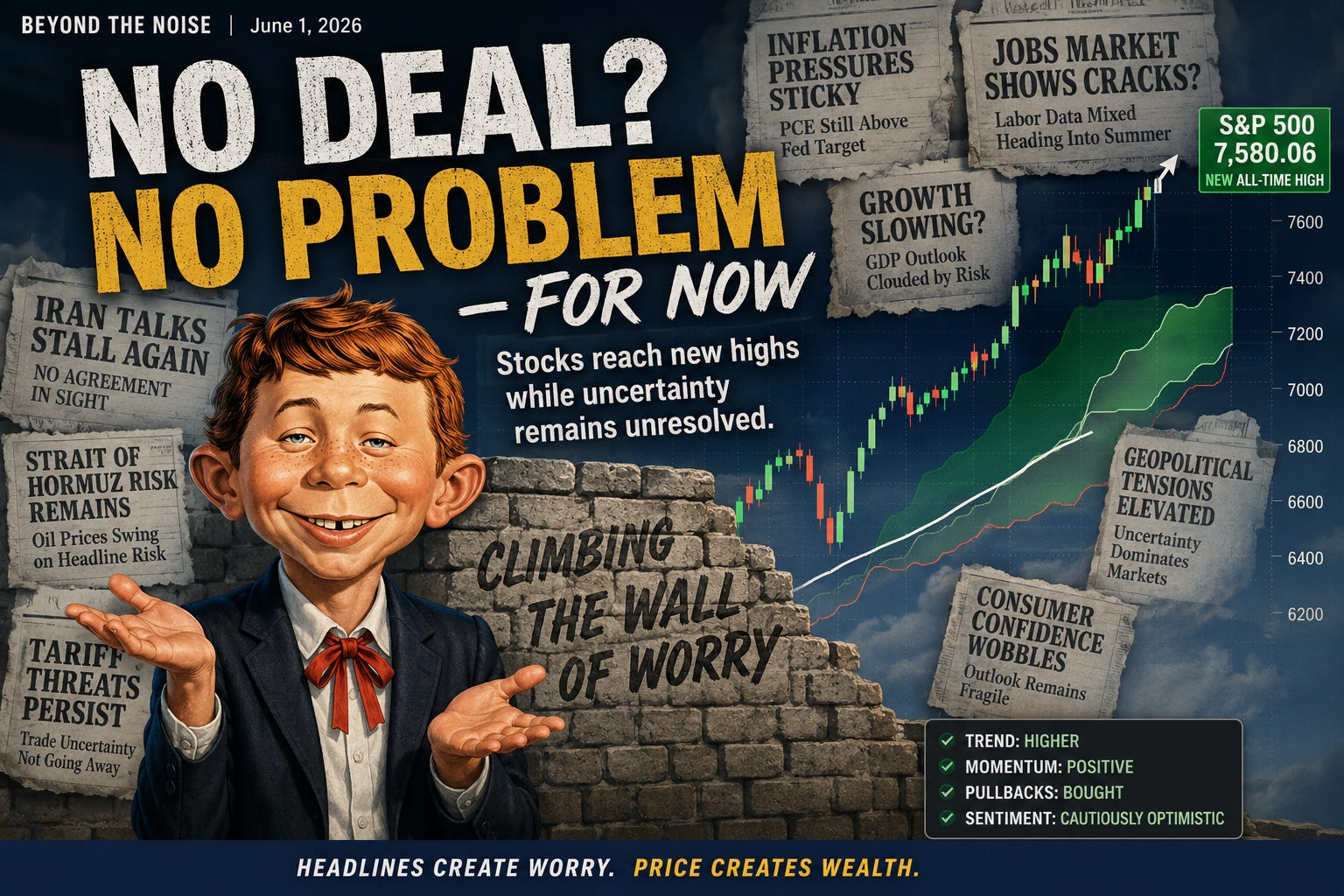

And yet the S&P 500 closed the week at fresh all-time highs, with technology once again leading the advance.

At some point, traders have to acknowledge what price is saying.

Whether investors agree with it or not, the market is currently behaving as though the path of least resistance remains higher.

And until price proves otherwise, that deserves respect.

The Market’s Message Hasn’t Changed

For weeks, investors have been conditioned to expect that some combination of geopolitical tension, inflation concerns, or economic weakness would eventually derail the rally.

Instead, every pullback has been met with buyers.

Last week’s action reinforced that theme.

The market opened the week with uncertainty surrounding ongoing U.S.-Iran negotiations. Headlines alternated between progress and setbacks, creating plenty of reasons for caution.

Yet by Friday, the S&P 500 had quietly pushed to another record close.

The message from investors appears straightforward:

No agreement is preferable.

A favorable agreement would be welcome.

But as long as conditions don’t significantly deteriorate, traders seem comfortable maintaining risk exposure.

That is a very different mindset than we saw earlier this year when uncertainty itself was enough to trigger aggressive selling.

Today, uncertainty is being tolerated.

And that subtle shift in psychology matters.

When Markets Stop Waiting

One of the more interesting developments over the past month is how quickly markets have moved from worrying about potential outcomes to discounting them.

Investors are no longer waiting for perfect clarity.

They’re making assumptions.

The current assumption appears to be that:

Iran tensions remain contained

Energy markets remain functional

Inflation pressures remain manageable

The economy slows, but doesn’t break

Could any of those assumptions prove wrong?

Absolutely.

But markets don’t trade on certainty.

They trade on probabilities.

Right now, investors appear comfortable assigning relatively low probabilities to worst-case scenarios.

That helps explain why stocks continue moving higher despite headlines that would have created far greater anxiety just a few months ago.

Technology Continues to Lead

Another notable feature of this rally is who continues to lead it.

Technology remains firmly in control.

The Nasdaq gained roughly 8% during May, significantly outperforming many other sectors.

AI-related spending themes remain intact.

Earnings expectations remain strong.

And investors continue rewarding companies with visible growth trajectories.

That leadership matters because healthy bull markets typically require leadership.

For now, technology continues providing it.

As long as capital keeps flowing toward growth-oriented sectors, it’s difficult to build a strong bearish case against the broader market.

The Technical Picture Remains Bullish

The chart continues telling a constructive story.

The S&P 500 successfully tested cloud support during the April correction and has been advancing steadily ever since.

The trend remains firmly intact:

Price remains above the cloud

The 50-day moving average continues rising

The 200-day moving average continues rising

Momentum remains positive, although no longer accelerating

Most importantly, there is still little evidence of sustained institutional selling.

Instead, the market continues displaying the behavior we’ve discussed repeatedly throughout this rally:

Pullbacks are opportunities.

Not warnings.

At least for now.

Eventually that behavior will change.

But there is little evidence that change has begun.

This Week: Employment Takes Center Stage

While geopolitical headlines will continue attracting attention, the economic calendar becomes more important this week.

Several employment-related reports could influence expectations for growth, inflation, and Federal Reserve policy.

Key reports include:

Tuesday

JOLTS Job Openings

Wednesday

ADP Employment Report

ISM Services

Thursday

Weekly Jobless Claims

Friday

Non-Farm Payrolls

Unemployment Rate

Average Hourly Earnings

Employment data remains one of the most important pieces of the macro puzzle.

Markets continue searching for evidence that the economy is slowing enough to keep inflation under control, but not slowing enough to threaten earnings growth.

That balance remains critical.

A “Goldilocks” labor market remains the ideal outcome.

The Psychological Challenge

The hardest part of this environment may not be analyzing the market.

It may be trusting what the market is saying.

Many traders remain anchored to risks that have not yet materialized.

Others remain convinced that record highs automatically imply danger.

Sometimes they’re right.

But trends often persist far longer than logic alone would suggest.

The market doesn’t require universal agreement to move higher.

In fact, rallies often thrive when skepticism remains abundant.

The question every trader should be asking right now is simple:

Am I trading the market I see, or the market I expect?

That’s an important distinction.

Because right now, the market continues rewarding those willing to follow price rather than argue with it.

The Bottom Line

The market entered the year facing concerns about inflation, tariffs, economic growth, Federal Reserve policy, and geopolitical conflict.

Many of those concerns remain unresolved.

Yet stocks continue making new highs.

That doesn’t mean risk has disappeared.

It simply means investors currently view those risks as manageable.

For now, the market’s verdict is clear:

No deal? No problem.

At least not yet.

The trend remains higher.

Momentum remains constructive.

And until price starts telling a different story, disciplined traders should continue respecting what the market is actually doing rather than what they think it should be doing.