Continued Rotation Over Resolution

A Sideways Market, a Policy Week

Beyond the Noise

Continued Rotation Over Resolution

January 25, 2026

Market Recap — Rotation Still Doing the Work

U.S. equities ended last week largely unchanged at the index level, but once again the real story was beneath the surface.

The S&P 500 continues to consolidate near highs, digesting gains rather than extending them. Underneath that sideways action, capital continues to rotate — favoring more defensive, cash-flow-oriented areas while select growth and momentum names cool. This is not a risk-off tape. It’s a re-positioning tape.

That distinction matters. In environments like this, broad index exposure tends to stall, while individual stocks with specific catalysts, valuation resets, or supply-demand tailwinds continue to move independently.

Dispersion remains the defining feature.

Looking Beneath the Index

Last week reinforced that theme. Some sectors worked, some stalled, and others chopped — exactly what you’d expect from a market pausing at elevated levels rather than rolling over.

That’s also why stock selection continues to matter more than macro guessing. Rotation favors patience and selectivity, not urgency.

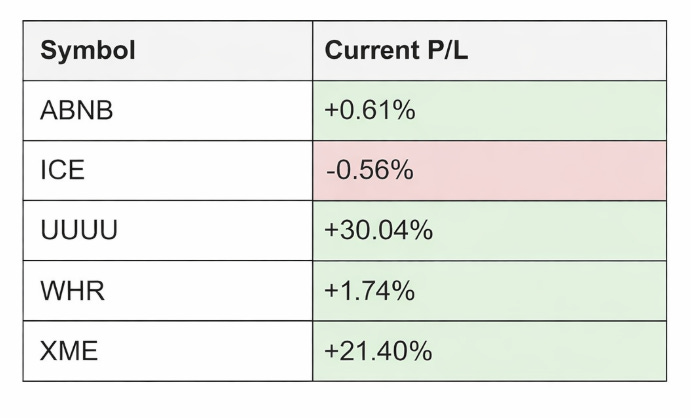

FMT Open Stock Picks Snapshot

Below is the current snapshot of open FMT stock picks:

These positions are not expressions of a single macro call. With the partial exception of materials, they represent company-specific opportunities working inside a range-bound index environment — exactly the type of setup that tends to perform best when indexes compress.

What Matters This Week — FOMC Takes Center Stage

From a pure data standpoint, the economic calendar is relatively light. That puts the spotlight squarely on Wednesday’s FOMC decision and press conference.

The Fed is widely expected to hold rates steady. As usual, the market reaction will hinge less on the decision itself and more on tone, language, and forward guidance:

Any emphasis on patience or data dependence will be scrutinized

The balance between inflation progress and labor resilience remains key

Markets will listen closely for clues around the timing — or lack thereof — of future cuts

Outside the Fed, attention will also drift toward:

Earnings season, particularly guidance from large-cap and cyclical leaders

Housing and labor data that feed the soft-landing narrative

Ongoing geopolitical risk, including Iran tensions and unresolved trade and tariff questions

The Supreme Court’s pending tariff-related rulings, still a background risk for materials, industrials, and global supply chains

In weeks like this, price reaction matters more than headlines.

Macro takeaway: If data leans stronger than expected, Powell’s forward guidance may err on patience, not cuts. Weak data could amplify expectations for cuts later in Q1/Q2.

📈 Major Earnings This Week

This is one of the most consequential earnings weeks of the quarter:

🗓 Earnings Highlights by Day

(Note: Pre-market open/after close flags are from aggregated earnings calendars.)

Monday, Jan 26

Steel Dynamics (STLD), Nucor (NUEN), Graco (GGG) — early industrials data points.

Tuesday, Jan 27

American Airlines (AAL), Boeing (BA), Northrop Grumman (NOC), Texas Instruments (TXN), Seagate (STX) — cyclicals and industrial tech.

Wednesday, Jan 28

🚨 Fed day + Big Tech

Microsoft (MSFT)

Meta Platforms (META)

Tesla (TSLA)

All three are expected to be market placards of sentiment post-open/after close — likely headline drivers depending on guidance.

Thursday, Jan 29

Apple (AAPL)

Caterpillar (CAT), Mastercard (MA), Honeywell (HON) — cyclicals + mega-caps.

Friday, Jan 30

American Express (AXP)

Chevron (CVX), Exxon Mobil (XOM) — financials and energy.

🧠 Earnings Narrative to Watch

Tech leadership or further rotation? Weak guidance from MSFT/META/AAPL could reinforce the late-cycle rotation theme.

Cyclicals & industrials (BA, CAT, NOC) may confirm broader economic momentum or slowdown.

Financials/energy will test whether defensive dispersion persists into sectors traditionally tied to growth or commodities.

Guidance from these names will help determine whether leadership rotates back toward mega-cap growth or continues to broaden into cyclicals, industrials, and value-oriented areas.

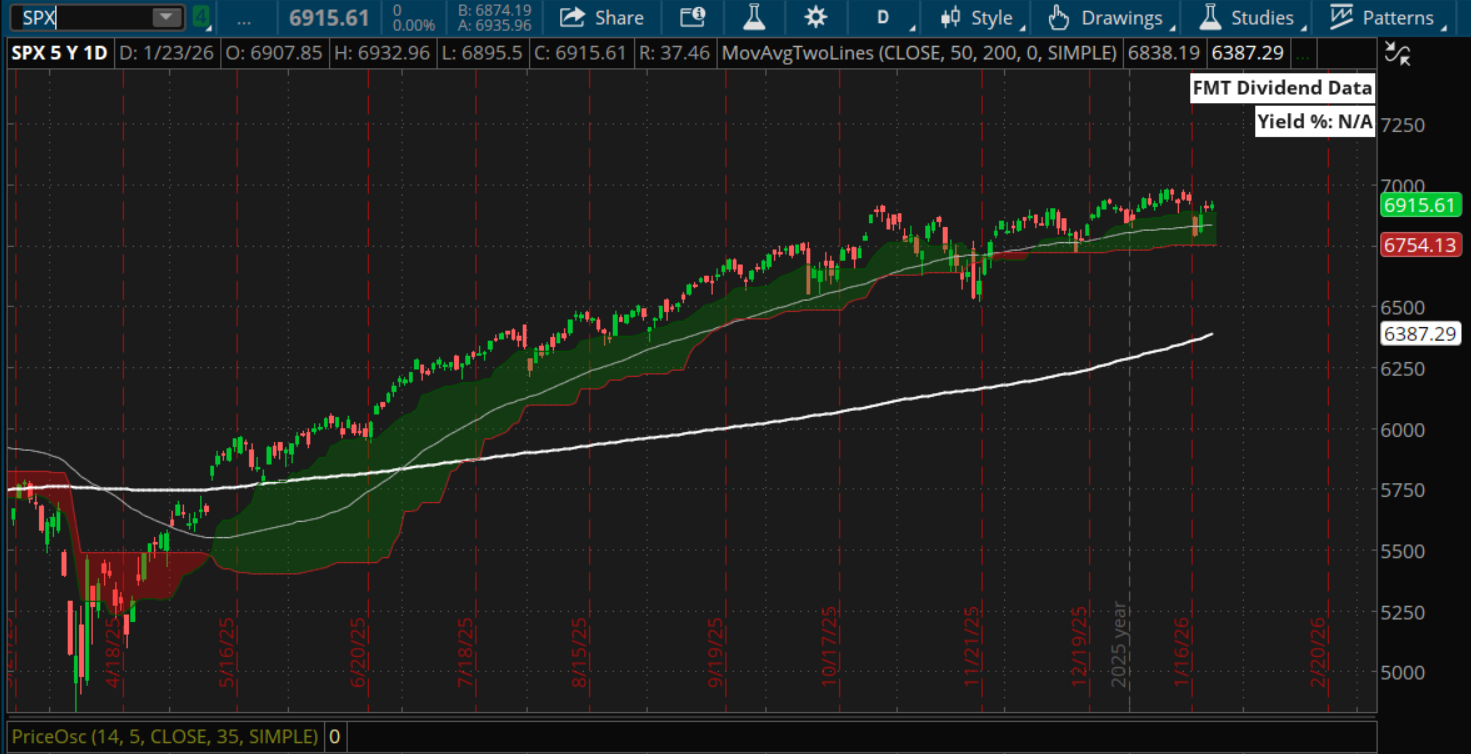

Technical & Sentiment Context — 50-Day Still the Line

From a technical standpoint, the S&P 500 remains in a constructive consolidation.

The 50-day simple moving average continues to be the key support level to watch. Price briefly pierced that level during the Greenland-related geopolitical flare-up, but once those concerns were tamped down, buyers stepped back in and reclaimed it.

That behavior reinforces the idea that this is a pause, not a breakdown.

As long as the index holds above the rising 50-day, the primary trend remains intact and favors rotation, digestion, and selective continuation rather than aggressive downside.

🎯 Trader’s Playbook

Expect continued chop at the index level

Respect the 50-day as the tactical line in the sand

Favor individual names with clear catalysts over broad bets

Don’t chase strength in crowded trades

Let rotation — not urgency — do the work

In markets like this, discipline matters more than prediction. Sideways indexes with expanding dispersion can be frustrating — but they’re often where the best opportunities quietly develop.

Yeah, more of a re-positioning tape rather than a risk-off market, especially when dip buyers have been rewarded constantly for the last several years. Why change now?

And I've also noticed the 50-day as a practical line in the sand.

And also, the importance of stock selection, catalysts, and rotation.